Biotech Roundtable: The Quest for Translation

Facing mixed market signals, biotech companies look to rise above the fray in advancing new-wave discoveries to the clinical finish line.

Amid all the hustle and bustle at the recent JP Morgan Healthcare Conference, the industry’s largest annual confab for hopeful dealmakers, Pharm Exec, with support from health communications agency Russo Partners, convened a roundtable discussion with CEOs from seven emerging biotechs to explore the prevailing issues and challenges facing the biopharmaceutical sector in 2017. Does true innovation-or the potential of new technologies and novel science in transforming medicine-still hold the trump card to opportunity in today’s turbulent and uncertain healthcare, business, and regulatory climates? Staying above the fray will be key to pushing hopeful new biomedical discoveries to the clinical finish line.

PE: We wanted to get a well-rounded perspective on the state of biotech at the moment from a diverse representation of companies in this space. Could you describe what is unique about your respective organizations?

JIM JOYCE, Aethlon Medical: We are a clinical-stage organization that is advancing a therapeutic biofiltration device that has a specific affinity to bind circulating viruses and cancer-promoting exosomes, based on the unique structure that resides on the surface of these disease targets. We are in a feasibility study with the FDA-a modular study that allows us to branch off into multiple viral targets. The exosome field is emerging on both the therapeutic and diagnostic fronts. Beyond our efforts to target tumor-derived exosomes, we have been advancing a candidate exosomal marker to detect

and diagnose chronic traumatic

Photos: Joseph Schell

encephalopathy (CTE) in living patients. A former teammate of mine (Joyce played football at the University Maryland and briefly with the Denver Broncos in 1984-85) passed away in 2008, and he became the second person diagnosed with CTE by the Boston University CTE Center. Based on our knowledge of exosomes, we were invited to participate in the first NIH study of CTE. The most high-risk group to suffer from CTE is former NFL players.

In this study, we demonstrated that exosomal tau, which we call a TauSome, might provide a means to monitor the abnormal accumulation of tau protein in the brain, which is the hallmark of CTE. We were able to demonstrate that TauSome levels were significantly higher in subjects who played in the NFL as compared to controls from the same age group. We also observed that cognitive decline seemed to correlate with high TauSome levels.

CHRIS ANZALONE, Arrowhead Pharmaceuticals: We are a RNA interference (RNAi) company focused right now primarily on hepatitis B and alpha-1 antitrypsin deficiency. We also have a program, ARO-F12, for thrombosis and angioedema. We’ve got some oncology programs as well.

JIM McGORRY, Biostage: We’re a regenerative medicine company focused on esophageal cancer, a silent killer. The disease afflicts about half-a-million people annually worldwide. In the US, there are 17,000 new cases reported each year and 15,000 deaths from the disease. The standard of care for a patient is to undergo an esophagectomy, in which all or part of the esophagus is removed. This leads to the need for the patient to undergo a gastric pull-up, which is predictably medieval. The alternative is a colon interposition, in which the colon is used to replace the esophagus. The five-year survival rate for these patients is 15%. We are focused on improving the therapeutic options for these patients.

Our Cellframe technology uses the patient’s own mesenchymal stem cells that are adipose-derived from a biopsy. We isolate and extend the mesenchymal stem cells and put them onto a synthetic scaffold. The implant is placed where the tumor was removed. After 21 days in the patient, we remove the synthetic scaffold, leaving only a regenerated, fully functioning esophagus. We hope to file an IND (investigational new drug) with the FDA this year, as well as proceed into human clinical trials.

GEORGE YEH, TLC Biopharmaceuticals: Fundamentally, we are using lipid nanoparticles to deliver drugs more effectively. That is, we can create more targeted drugs as well as those designed for longer duration. The areas we cover include oncology, where we can use these nanoparticle delivery systems to not only package many small molecules but also coat these nanoparticles with antibodies on the surface. Not only is the drug going to the tumor site, or where we may want the drug to go in a tissue, but it can also be directed into a specific compartment within the cell. We’re looking to target specific molecules in specific compartments as well; that is another program still at the discovery stage. In the area of pain management, we have one program currently in the clinic in osteoarthritis.

CHRISTIAN KOPFLI, Chromocell: Chromocell is a 15-year-old company. We started with a platform technology, called Chromovert. Chromovert allows us to create hard-to-express human receptors, such as for taste, pain, heat, etc. We used these receptors to do high-throughput screening to find new molecules that stimulate or block these receptors. For example, finding a molecule that stimulates the sweetness receptor, or a molecule that blocks the pain receptor. Initially, we focused on taste receptors and worked with consumer-goods companies to find new sweetness or saltiness enhancers. While we built our flavors business, we used a portion of the income to go into pain research, focused on a target called NAV1.7, a pain receptor.

The interesting thing about NAV1.7 is that it’s highly validated genetically and it’s a non-opioid receptor. We developed that receptor and did a high-throughput screen to find a molecule that blocks the NAV1.7 pain receptor. After development of the molecule, in 2015, we got closer to the stage where we thought we had a valuable asset. We partnered this program with Astellas Pharma and entered into clinical trial with our new pain medication in 2016.

DANIEL ZURR, Quark Pharmaceuticals: We are strictly in small-interfering RNA (siRNA). We now have the most robust siRNA clinical pipeline in the world. We have two products in Phase III trials and three in Phase II. We also received the approval to start dosing patients in India and China. We had to teach the authorities there what “siRNA” is. They told us that it would be difficult, but we overcame the difficulties and are dosing patients there. Two out of the five indications are for delayed graft function (DGF) for kidney injury and three are for ischemic optic neuropathy (ION), which is a rare disease, and age-related macular degeneration (AMD) and glaucoma.

GIL VAN BOKKELEN, Athersys: We are a company that is focused exclusively on regenerative medicine. We have developed an off-the-shelf stem cell therapy-stem cells in a vial. Unfortunately, bone marrow transplantation, which has been around since the late 1950s, is a complicated, messy, and not very scalable procedure. What we do is take a special class of stem cells, which we can isolate from young, healthy, consenting donors. We have shown that these cells have very robust growth properties. We can expand them to produce the equivalent of millions of clinical doses with a small amount of material from a single donor, and can do this consistently across donors. We have also demonstrated clinically in six different programs that we can administer these cells like type O blood. We don’t have to tissue-match or immunosuppress the patient we put the cells into.

Our most advanced program is headed into a pivotal Phase III study. We recently got FDA authorization to conduct that trial under a special protocol assessment (SPA). Our lead indication is in treating ischemic stroke. The study will be conducted in the US, Canada, and Europe. In parallel, we’ve got a partnership in Japan to take advantage of the new regenerative medicine accelerated regulatory approval pathway there. We also have Phase II programs for treating damage from myocardial infarction and treating acute respiratory distress syndrome.

PE: Regarding the US, specifically, do you feel the recent sentiments expressed by the Trump administration on the industry in areas such as pricing and overseas manufacturing will fuel significant volatility in the biotech space this year?

JOYCE: I think it’s going to be somewhat unstable. You have an administration whose background is not in this industry. There was some early dialogue around the question of who will be the representatives in the new administration providing oversight for the biotech industry. A lot of those questions haven’t been answered yet. There are a lot of unknowns, such as who is going head the FDA?

VAN BOKKELEN: One of the things that we’ve seen consistently over the past few decades is that the market will always reward innovation, regardless. If you develop a solution that is addressing an unmet medical need-where patients really need it-and do it in a way that demonstrates safety, real therapeutic effectiveness, and practicality, then the market embraces that and innovative organizations get rewarded for that.

JOYCE: The president has discussed slashing drug prices extensively. People can look at the statistics on what it costs to commercialize a drug, from R&D through approval. Whether it’s the Tufts University statistic of $1.6 billion or somebody else’s statistic that says it’s over $2 billion, none of those take into account the cost of the failures. From a pure business standpoint, the new administration or others who don’t follow this space need to understand what the real cost and barriers to entry are and that those barriers are a factor in determining pricing.

ANZALONE: The flip side of that coin is that it’s incumbent upon all of us to educate the broader public and, likely, the administration as well that Valeant and [former Turing CEO] Martin Shkreli are not our industry. Those are not representative of what we do. The vast majority of us are doing things that are not just innovative but are potentially revolutionary from a health standpoint. They are not incremental gains; they are switches on and off. Those have costs-and most of those fail. The extent that we can help people understand this, the better off we are.

KOPFLI: I have the impression that the mood was becoming a little friendlier than last year-it was going up. I thought maybe the election outcome actually played a part in that-that people thought that price controls were a little bit more associated with Hillary Clinton. That was my conclusion, but now I’ve been

proven wrong on that. I think the president tweets out things and then he oftentimes comes back with other ideas. I wouldn’t over-interpret any of this until the dust settles.

McGORRY: In addition to innovation, we need to focus on the price and the outcomes of our evidence-based medicine. At the end of the day, our value is in solving unmet medical problems. I fear that the industry’s reputational challenges are going to get in the way of a small innovative company trying to move a program forward, because they are associated with areas or individuals that, unfortunately, may act as a barrier.

PE: What are the things your respective leaderships think about or do actively-on a short- or long-term basis-to reinforce or improve the industry’s reputational component?

McGORRY: As a small company, Biostage hopes to improve the reputation of the industry by focusing on innovative technology, making wise business decisions, and learning from our peers. We hope to continue to make a difference in patients’ lives.

VAN BOKKELEN: The organizations that we might be members of, whether it be the Biotechnology Innovation Organization (BIO) or the Alliance for Regenerative Medicine (ARM), or others, they don’t just include companies. In the case of ARM, it’s also disease foundations, patient groups, a broad community of people that all want the same thing. They want safe, effective medicines to be developed and made available, and, therefore, are working together. One of the ways in which you can do that and make it impactful is to utilize different vehicles and platforms. For example, through the use of video, you can tell a story to personalize and humanize just how debilitating or devastating a particular disease indication might be and how innovation can actually help address that.

So, part of this is just good, old-fashioned communication using sophisticated, new-age technology platforms to help us do that on a more effective and comprehensive basis. Because, frankly, that’s one of the things we all need to be devoting a little bit more time and effort toward-to help the outside world understand just how important and significant the work that we’re doing really is.

KOPFLI: I think we all need to use the new tools to effectively communicate. I believe that one of the problems we have as an industry is that people have misconceptions about the industry. One idea may be that the patient side become more active-patient advocacy groups and the doctors who use the products we develop. We are innovating, but we are also creating profits, and, thus, our message might not resonate as much. Maybe people that benefit from the innovative products can step up more and help us communicate the message.

McGORRY: Every company expresses patient interest in a different way, but perhaps we need more dedicated people working in this area. Patient-centric approaches to business, such as collaborating with patient advocacy groups, are critical. They help give the business a deeper purpose.

PE: Stemming off this whole discussion of reputation, does the industry need to do a better job, perhaps, in regulating itself when it comes to things like pricing? Is that something that’s even possible?

YEH: I think I can provide a different perspective, coming from Taiwan or Asia. When looking at the overall market, you start to see the money flow when you’re talking about capital markets. We are actually seeing a lot of capital flowing into the US right now. That will help drive up the whole market this year. Second, even though Trump talked about pricing and things like that, if you think about what is really driving the innovation, it’s actually about how you can get better pricing in the US. Anyone, no matter where they are, who wants to make an impact in the healthcare industry, they come to the US. I’m personally optimistic about this year and going forward, based on the capital market, the money flow, and what is driving this industry. Trump can tweet whatever he wants, but I think these are the key drivers.

ZURR: Why do you think more money will come from the Far East this year compared to last year?

YEH: When the currency starts to fluctuate locally, you want to go to much more stable and stronger currency. And if you are talking about tax reduction in the US, if you look at a big corporation, right now the corporate tax is 35%. If you just go down 10%, everybody’s EPS, in general, is going to increase 20% automatically. That’s if your gross still stays the same.

PE: Are there other regions where you are seeing solid industry growth in the early stages of 2017?

McGORRY: When I think about growth within our area of esophageal cancer, it comes down to epidemiology. This disease is 10 times more prevalent in the Asian population. Food and diet in regions outside the US and Western Europe is a contributing factor to a much higher incidence of esophageal cancer. Therefore, we are focusing on the Asian market due to the increased prevalence of the disease in those populations.

VAN BOKKELEN: The epidemiology is definitely a big consideration when you are thinking about moving into a particular geographic region or about incorporating clinical activities in those areas. A region that I have been very impressed with and spent a lot of time in, is Japan. One of the thrusts of Abenomics is to invest more in healthcare and particularly innovative technologies like regenerative medicine. Japan, like a lot of other countries around the world, is experiencing an unprecedented transition where we are seeing a massive expansion of the elderly segment of the population. A lot of people haven’t really taken the time to assess what that is going to mean from a healthcare economic perspective.

The reality is that as we get older, we can spend eight to 10 times more annually on healthcare-related expenditures than we do when we are younger and healthy. Japan has the worst demographic profile of any developed country and probably any country, period. They recognized this because they’ve got a national healthcare system, and they started doing things that have created a much more favorable environment, designed to promote innovative healthcare solutions in the areas where they need them the most. Within the last couple of years, Japan has implemented new regulatory frameworks designed to expedite development, not just for regenerative medicine therapies but other forms of innovative therapies, which I think have a more broad-based benefit in terms of shortening the clinical development path, making it more concise, more efficient, and yet doing it in a way that protects and ensures patient safety and well-being.

If you can create better efficiency, which some of the provisions of 21st Century Cures Act in the US are designed to do, and if some of these other regulatory initiatives have the desired impact in that regard, you can get a shorter and less expensive development cycle. Ultimately that benefits everybody-the companies, the patients, and the investors.

JOYCE: One of the most challenging things that management of a therapeutic company faces is the question of what regions of the world are they going to pursue. In our case, we had opportunities to initiate human studies early on in India and other regions. The regulatory barriers were lower in those regions. There was never any assurance that the FDA was going to give us clearance to initiate studies in the US, so we focused on collecting data overseas. It was very valuable. That data got us to the point where the FDA approved studies for us to move forward and advance our technology in the US.

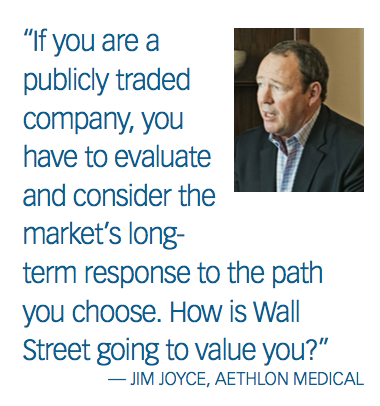

Then you have the dilemma of thinking about, “Well, am I going to focus on US clinical progression?” If you are a publicly traded company, you have to evaluate and consider the market’s long-term response to the path you choose. How is Wall Street going to value you? Some companies may choose to say, “We want to focus on early product commercialization”-a lower-barrier entry-and can be successful in doing that, with the plan of coming back and

advancing things in the US. But then they find out that Wall Street starts to value them on a revenue earnings model once their product is approved overseas. And, thus, their post-approval shrinks to levels below that of when they were progressing clinically.

It’s a very challenging decision. It’s a decision that most investors don’t understand. You need to evaluate where the primary market is, what’s the largest market, what is the reimbursement climate, and where the value is. If you are a company that is doing something that could attract large organizations that might want to acquire your business, if you are not advancing clinically in the US, there is probably not much interest. I have seen colleagues go overseas, never to be seen again. And I have seen companies here in the US take therapeutic candidates through the FDA approval process and fail.

ANZALONE: I disagree with one of the things you said. I think, dependent upon where in the world a company’s clinical development is happening, you can still get a lot of interest from Wall Street and still be taken seriously from acquirers. It depends on where it goes. It’s been our experience that the way the FDA is structured now, that-at least for us-there is little reason to do early stage clinical development in the US. It’s much faster ex-US. It’s easier for FDA to have it done ex-US and then come back here for pivotal studies.

ZURR: Nevertheless, if you develop a really innovative drug for an unmet medical need, if you don’t get FDA approval for the clinical studies, you will not go to a country like India. Getting US approval is still the gold standard. You can conduct some studies outside the US and return to the US later. But if you want to get approval worldwide, you had better do it in the US first.

YEH: We have trials done in Japan, China, Taiwan, Europe, and the US. I always tell people the fastest way is through the Taiwan FDA or the China FDA or through the NDA (new drug application) process with the US FDA first. Because, with a lot of these other countries, there are not as many experienced reviewers, which can make the process very indecisive and go in circles.

PE: In the US, to what level do you believe the “Cures” legislation, when implemented, will truly help achieve the changes sought in streamlining the regulatory process and ultimately accelerating drug development?

McGORRY: It will be interesting to see how other government agencies become involved after the Cures Act. Before a company begins discussions of reimbursement, the FDA will provide vouchers and incentives to companies that focus on tropical diseases and pediatric diseases. I’m hesitant to encourage other government agencies to define innovation in drug

development through incentives. There need to be some incentives, but this is a cautious area.

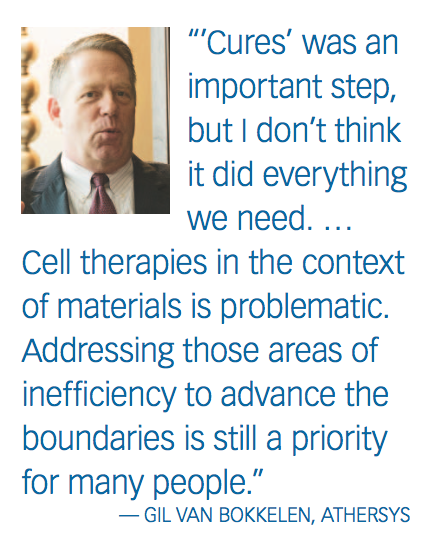

VAN BOKKELEN: Cures was an important step in the right direction, but I don’t think it did everything we need. The next phase in the legislative landscape is going to be the PDUFA reauthorization and putting some additional provisions and mechanical things in place that will help us continue that trend toward hopefully a clearer, more predictable, and more efficient regulatory framework for all of us. There’s been a particular challenge at the agency with combination products. Cell therapies in the context of materials is problematic. So, addressing those areas of inefficiency to advance the boundaries is still a priority for many people.

PE: To that end, is the merging of different review departments within FDA a wish during a product evaluation-so that you don’t have 16 people in the room, so to speak?

McGORRY: The FDA is right to have a delineation of departments to regulate a device versus a biologic. This enables regulators to stay ahead of the technology and make an informed decision about the potential of the product.

The difficulty comes when the FDA evaluates products that address rare or orphan diseases. Today, there are thousands of orphan diseases identified around the world. With that in mind, there is an important social question: should we focus our efforts on treatments for just those rare diseases or focus our efforts on treatments for broader disease states? This social question also applies as technology and big data change.

PE: Regulatory burden aside, what are some of the main scientific challenges your companies face in advancing your technologies forward? Is it achieving new modalities of medicines, like stem cell or RNA therapies? Is it finding new targets?

ANZALONE: We have enough science to fill all of our lifetimes. It is translating that into clinical programs and then translating that into marketable products. We are at this amazing time in science where we can innovate extremely rapidly with animal models, in vitro, etc. But there is still this massive bottleneck, in part because it’s complicated now to get into clinical studies, but also because of the capital necessary to support it.

KOPFLI: I couldn’t agree more. There’s plenty of science and technology out there. It’s more about choice-where are you going with it? The reimbursement factor is important as well. You go into something with big hopes, but very early on in the process, you have to consider the market outlook; does the product you are trying to develop really compare sufficiently above the what’s out there? That may sound easy to do at first glance, but particularly in my company’s area-pain, it’s so broad and risk profiles come into play. The reimbursement aspect can also put you in a situation where you believe in that molecule or that therapy but just can’t be sure whether it will get reimbursed or whether the insurer understands that it should be reimbursed. These are all factors that you need to take into consideration.

VAN BOKKELEN: There is a lot of debate right now about how do you appropriately reimburse so-called curative therapies. Some of these are designed to be a one-time therapy that has a long-lasting therapeutic impact in a way that’s not contemplated under the historical third-party payer reimbursement dynamic, which is “we are going to pay for you to take this pill for an extended period of time, or forever.”

To use some of the pediatric orphan indications, for example, where you can treat a child and cure a disease that might otherwise be progressive and debilitating, that has decades-long impact; but, yet, you’ve only got a small population and you still have the significant cost and development challenges to face. How do you figure out a reimbursement dynamic that’s going to accommodate all of that? The reality is we still don’t know. There is discussion going on between industry, third-party payer groups, and sponsors and innovator organizations like ARM and BIO to try to get to a better place on this issue.

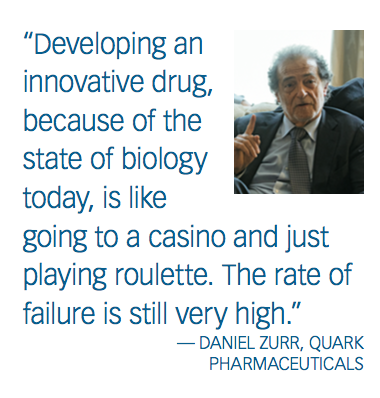

ZURR: Developing an innovative drug, because of the state of biology today, is like going to a casino and just playing roulette. The rate of failure is still very high. It’s true that there are more technologies, and from time to time, like in every science, you have one breakthrough, such as CRISPR/Cas9, for example, and that moves everything forward. There are certain drugs today that you have to test diagnostically before administration in humans. These are the directions

that we’re heading.

PE: What’s the catalyst for these personalized approaches? Is it eliminating a failure faster? Is it artificial intelligence that can help make better and earlier predictions of effectiveness?

VAN BOKKELEN: Our ability to assess and analyze genetic heterogeneity has improved by leaps and bounds over the past decade. I’m not saying it’s perfect, but we now have much more comprehensive knowledge about the human genome and some of the things that are important from a clinical perspective. It hasn’t been implemented to the point where we can routinely anticipate and characterize those types of things clinically. But the technology has clearly advanced in that direction.

JOYCE: Think about how interesting it would be if you could obtain regulatory answers quicker or understand whether your product is performing well sooner. In the case of a biotech company that is burning $5 million a month, what if you could get your answer six months earlier? That’s a lot of money saved.

VAN BOKKELEN: If you can help people get the answers faster in particular areas, there’s a lot of value in that. Achieving clarity faster and more efficiently is important.

McGORRY: There is an analysis of drugs on the market that compares their original indications to their marketed indication, showing that likely more than half were approved in a different indication than originally planned. By predicting effectiveness, or lack thereof, earlier, we can improve drug development. Some people say it’s not that the drug fails; it’s that the company fails the drug.

PE: Given these dynamics, how would you assess the state of emerging research areas such as stem cells, regenerative medicine, RNA technologies, etc.?

VAN BOKKELEN: I think that regenerative medicine, cell therapy and other advanced therapies, like gene therapy, are in a positive place right now. Contrary to a lot of the narrative out there, the FDA actually has significant knowledge and willingness to engage with companies and help give them guidance, much more than it did 10 or 15 years ago when this field was really just beginning, and in its early stages. This doesn’t mean that everything operates perfectly.

But I think that if you look at the capital flow into regenerative medicine and advanced therapies over the past several years, it’s risen dramatically. There’s a growing recognition and appreciation that this is one of those areas that could really transform medicine as we know it, particularly for some major problematic conditions where there are no effective solutions and no good current standard of care.

The challenge now in this space, as more of us are entering into late-phase clinical development, is to see those discoveries translated and see a few compelling cases go to the finish line. That would create a kind of tidal-wave phenomenon, if you will, pushing in the right direction. I think we are almost at that point.

ZURR: If you look at RNA, especially siRNA or microRNA, the antibody is part of the sophisticated immune system, which was discovered even before the innate, or primitive, immune system. And we now know the role that RNA is playing in our body. One of the biggest surprises after the mapping of the human genome was that we have almost the same number of genes as the mouse. So, what is the difference? The difference is the regulation of the genes-and RNA is the major regulator.

The human race is able to take the antibody, which is a part of our immune system, and manipulate it to produce efficient drugs for its own advantage. Similarly, we are going to do that with the primitive immune system of siRNA. It’s just a question of time. Once the first siRNA hits the market, you will see an avalanche.

Addressing Disparities in Psoriasis Trials: Takeda's Strategies for Inclusivity in Clinical Research

April 14th 2025LaShell Robinson, Head of Global Feasibility and Trial Equity at Takeda, speaks about the company's strategies to engage patients in underrepresented populations in its phase III psoriasis trials.

The Misinformation Maze: Navigating Public Health in the Digital Age

March 11th 2025Jennifer Butler, chief commercial officer of Pleio, discusses misinformation's threat to public health, where patients are turning for trustworthy health information, the industry's pivot to peer-to-patient strategies to educate patients, and more.

Bristol Myers Squibb’s Cobenfy Falls Short in Phase III Trial as Add On Therapy for Schizophrenia

April 23rd 2025In the Phase III ARISE trial, Cobenfy administered as an adjunctive treatment to atypical antipsychotics for patients with inadequately controlled schizophrenia did not achieve statistically significant improvements.